Ingles Markets (NASDAQ:IMKTA) is a unloved, misunderstood, and just plain ignored grocery stock that has loads of hidden value hidden under the surface. A little investigation reveals it’s one of North America's cheapest stocks, if not the cheapest. The problem? The founding family sure doesn't seem very interested in unlocking any of that value.

Introduction

The Ingle family has a long history in the grocery business.

After working in his grandfather's grocery store in Asheville, North Carolina, as a young man, Robert Ingle was hooked. After doing a tour in South Korea during the Korean War and then graduating from university, he worked for a regional grocer before securing funding to carry on his grandfather's business. He opened his own store in Asheville in 1963, and Ingles was born.

Robert's strategy pretty much right from the beginning was to own the underlying real estate. Sure, this strategy would make it more expensive to expand, but it eliminates the risk of excessive rent hikes.

Remember, Sam Walton was forced to close down his first store after the landlord refused to renew the lease. It was a small town, so there were no alternate locations. Walton was forced to start over, and he learned a valuable lesson about controlling your own real estate. Walton was still happy to rent, but he signed a 99 year lease the next time around.

The company expanded from there, including buying a milk processing facility in 1982. This facility has undergone various expansions over the years, and production capacity has grown from 5M gallons annually to more than 60M gallons. This facility also produces bottled water, fresh juices, and other dairy products — which are sold in both Ingles and competing supermarkets.

It also opened a large distribution center, warehouse, and corporate headquarters in the outskirts of Asheville. This warehouse is located within 280 miles of even the furthest store, and spans 1.65M square feet.

These days, according to the company's latest 10-K, Ingles is the owner of 198 supermarkets located in North Carolina (75), Georgia (65), South Carolina (35), Tennessee (21), Virginia (1), and Alabama (1). Keeping with Robert Ingle's philosophy so many years ago, the company owns virtually all of its real estate. It owns the underlying real estate of 175 of its supermarkets, as well as 29 undeveloped sites in and around the cities in which it currently operates. As we’ll see, it also owns a bunch of additional real estate connected to and surrounding a number of its stores.

The stock is still controlled by the founding family. The original Robert Ingle has passed away, but he was replaced by his son, Robert Ingle II (better known as Bobby, to differentiate him from his dad). He controls 22.7% of all outstanding shares, including 72.5% of voting power. Class A shares are listed, while Class B shares carry outsized voting power. Ingle's ownership is concentrated in Class B shares.

Combined, there are a total of 19M shares outstanding. Approximately 14.4M of these shares are Class A shares, which trade freely. The other 4.6M shares are controlled by insiders -- mostly Ingle, but also other insiders. Bobby’s sister, Laura Lynn (who inspired the name of the company’s private label, called Laura Lynn) was a large Class B shareholder, but she sold off her shares over the years.

Class B shares are convertible to Class A shares at any time, providing insiders liquidity to sell their stock. Dividends are slightly less for Class B shares, those shareholders receive $0.15 per share each quarter. Class A shareholders get $0.165 per share on a quarterly basis.

Related: My closer look at Monarch Cement (OTC:MCEM), a similarly dirt-cheap, boring stock that’s worth a couple minutes of your time. It’s up ~20% since I wrote about it eight months ago.

Recent events

On September 27th, Hurricane Helene rocked Western North Carolina, causing considerable damage in the Asheville area.

Ingles was impacted by the hurricane in a few different ways.

Firstly, some inventory was destroyed. The company took a $30.4M impairment loss on that.

Secondly, the hurricane did damage to Ingles' facilities. The company recognized a $4.5M impairment on property damage in fiscal 2024, although it did receive $1M in insurance recovery funds in the first quarter of fiscal 2025.

The big impact was felt on the top line. Ingles reported $1.288B in sales in the three months ending on December 28th, 2024, compared to $1.481B in sales during the comparable period in 2023. That's a decline of more than 13% on a year-over-year basis, which is massive for a stable business like grocery. Business suffered as roads were closed and customers were displaced. Plus, it happened during the all-important Christmas quarter, a supermarket’s busiest time.

Profits plunged even further. Earnings per class A share were $0.89 in the most recent quarter, compared to $2.33 in the same period last year. That's a 62% drop.

The good news is most of the hurricane impact is in the past. The company incurred some $5.4M in cleanup costs in its most recent quarter, and four stores had enough damage that they needed to be closed. One is already reopened, while the other three are expected to come back online in 2025. There will be some costs associated getting these stores back up to shape, but the vast majority of hurricane costs have already been recorded. They're in the past.

Investors overly focused on the impact of Hurricane Helene have sent Ingles shares reeling, with the stock falling nearly 13% in the last six months. We'll note the huge selloff when the hurricane struck, the subsequent rally, and then another selloff. Shares are currently flirting with lows last seen immediately after Helene hit the Southeast.

This is great news for folks looking to take a long-term position in Ingles. Hurricane costs are just a distraction to the real thesis, which is just how valuable the underlying real estate is.

In fact, this real estate is so undervalued -- and so cleverly hidden -- that shares trade at a mere fraction of their true worth. Let's dive in.

Related: How I invest in REITs and how much I’ve realized that growth and quality management

A quick look at the real estate

Ingles does not disclose much about its real estate portfolio, but there's enough information there to piece together a pretty interesting picture.

First, a quick review. Ingles owns the following real estate:

1.65M square feet worth of warehouse and distribution facilities

A 145,000 square foot milk, dairy, water, and juice manufacturing plant

The underlying real estate of 175 of 198 stores

29 undeveloped sites

9.3M square feet of leasable space in shopping centres, of which 4.5M square feet is used by the company's supermarkets. So an additional 4.8M square feet of leasable space rented to third-party tenants

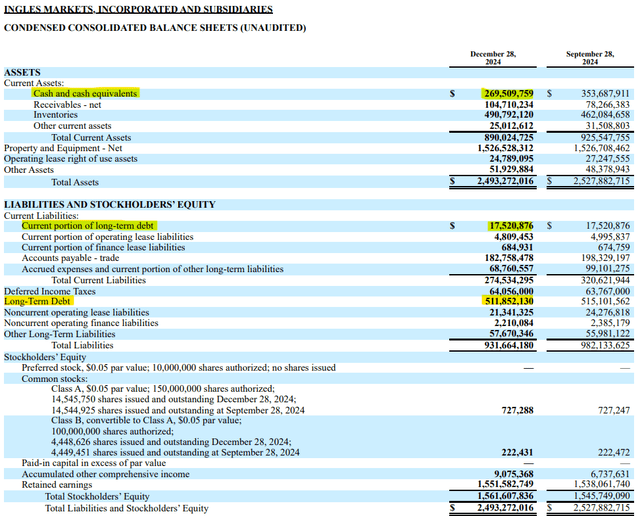

There is some debt owed against these properties, but the company doesn't separate what's real estate debt and what's debt used by the operating grocery business. We'll be conservative here and assume the entirety of the company's $529M in debt is owed against the real estate.

That's offset by the $269M in cash on the company's balance sheet, giving us a net debt position of $266M.

Here's a snapshot of the company's most recent balance sheet. I'm ignoring all assets and liabilities of the operating business because we want to focus on the real estate here.

Now that we've established the net debt against the real estate portfolio is worth $266M, now let's try to figure out how much the assets are worth.

To do so, I'm going to separate the real estate into three categories:

1. Industrial (warehouse and milk production space)

2. Ingles grocery space

3. Other retail space

Let's start with industrial. Between the two warehouses in Ashville and the milk production facility, Ingles owns 1.795M square feet of industrial space. These facilities are also sitting on approximately 130 acres of land, but we'll ignore that. Most industrial real estate sits on an excess amount of land, although not nearly as much as Ingles has.

As a comparable, we'll use EastGroup Properties (NYSE:EGP), which owns 63.1M square feet of industrial real estate, located in Sunbelt states like Texas, Florida, California, and North Carolina. It's not a perfect comparable, but it's close enough to be reasonable.

As it stands today, EastGroup has an enterprise value of $11B. Divide that by 63.1M square feet, and we get value of $174 per square foot. If we use that as a proxy for how much Ingles’s industrial real estate is worth, we end up with a value of $312M for the industrial property alone.

Next, we'll value Ingles's grocery space. As a reminder, it owns the underlying real estate of 175 of its 198 stores, but that doesn't tell us just how much real estate it owns.

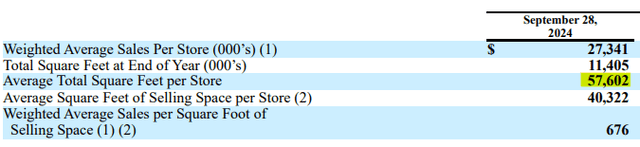

Luckily, the latest 10-k can help us out here. Ingles discloses that, on average, its stores are just a hair over 57,000 square feet. Multiply that by 175 and we get a grocery portfolio spanning 9.975M square feet.

Because there are no REITs that just rent out grocery space, we'll combine Ingles's grocery portfolio with the rest of its retail portfolio. Remember, Ingles owns an additional 4.8M square feet of space in retail developments that isn't rented to one of its stores. Add that to the grocery portfolio, and we get a total retail portfolio spanning 14.775M square feet. Let's round up ever so slightly, call it 14.8M square feet of total retail space.

Slate Grocery REIT (TSX:SGR.un) is a nice comparable here. It owns 15.3M square feet of gross leasable grocery-anchored real estate in the United States, a portfolio it values at US$2.4B. That works out to $146.40 per square foot. If we value Ingles's retail real estate per square foot at a similar level, it's worth $2.17B.

Put the two together, and Ingles's real estate portfolio is worth $2.48B. Take off the $266M worth of net debt, and we have a value of $2.21B for the entire real estate portfolio, net of debt.

(There's also the 29 pieces of land the company owns, which I'm not about to try and value. Consider that the "what you get for free" part.)

So, as it stands today, Ingles has a market cap of $1.2B, and it owns $2.21B in real estate once we net out the debt. That alone is a pretty compelling investment thesis, or so I would think. So not only are you buying real estate for fifty-five cents on the dollar, but you're also getting the grocery store operations for free.

It gets better. It turns out those grocery operations you’re getting for free are actually pretty good.

Reading this on the web? Get this article forwarded to you? Don’t forget to sign up for our FREE newsletter. Great stuff, just like this, straight to your inbox each and every Sunday

The operating company

I'm not going to spend much time on this part, since the real estate is the real star here. But I will say that at a $1.2B market cap, Ingles would be an interesting buy even if it didn't own any of its real estate.

Why? Because these guys are good grocers. They have consistently grown revenues and earnings over the last decade.

In fiscal 2015, Ingles generated sales of $3.778B and operating income of $137M.

Rather than use fiscal 2024 as a benchmark -- remember, the hurricane hit in Q4 2024 -- we'll use 2023. That year, Ingles generated top line revenues of $5.892B -- for growth of 56% in nine years -- and operating income of $289M. Operating income was up 111% in same period.

Operating income per share would be even better, since shares outstanding decreased by 6.2% during the last nine years.

Some of you might be arguing that Ingles over-earned during the pandemic. Profits on a per share basis essentially doubled during 2020, and kept marching higher in 2021 and 2022. The bottom line stepped back in 2023, and then dropped in half in 2024. 2025 won't be great either, with the impact of the hurricane hitting Q1 profits.

Earnings went much higher during the pandemic, but have fallen again

I'll also point out that Ingles was having a fine year in 2024 until the hurricane hit. It earned $2.33 per share in Q1. It did $1.72 per share in Q2. And it did $1.71 per share in Q3. That's $5.76 per share in earnings before Q4, which ended up at a slight loss because of hurricane impacts. But in 2023, the company earned $2.77 per share in Q4. So in a normal year, the company is quite profitable in the 4th quarter.

(Christmas, the most important holiday for a supermarket, occurs in Ingles’s first quarter)

I believe on a normalized basis -- i.e. 2026 -- the company can earn at least $8 per share in sustainable earnings, with that amount heading higher over time. That puts us at approximately 8x earnings today, which is obviously quite attractive. It's even better when we realize such an argument values the real estate at zero.

So, put it together, and the following for a fair value for Ingles:

An operating company worth 10x normalized earnings = $80 per share

Real estate worth $2.21B = $116 per share

Total value: $196 per share

Current price: ~$64

Upside to today’s price: > 200%

There's just one problem, and I'll cover it now.

Just how will the value be realized?

As mentioned, Ingles is controlled by Robert Ingle II. He's the chairman and largest shareholder of the Class B shares. He has 72% of voting control.

He's also incredibly media shy. The Ashville Watchdog tried to interview him for months, finally ambushing him at a bar where his band was playing cover songs. He didn't have much to say.

Ingle doesn't seem to have any desire to unlock any of this value. He just wants to sell groceries, and his dad taught him the best way to do that is to own the real estate.

So, this begs the question. Just how exactly does a value investor unlock all this hidden value?

I won't give anybody false hope. The answer is you don't. You wait for Bobby to figure it out. He's a grocer who has worked in the family business for a long time, so I doubt there's much desire there to quit. Even if he is in his 50s.

The good news is perhaps we don't need all that value to be crystalized for an investment to work out. Ingles should be able to create shareholder value by growing its top and bottom lines over time.

The company has a great balance sheet, so it should also be able to give back to shareholders. The ability to both buyback shares and pay increased dividends is there, and if I were the controlling shareholder, I'd use the company's money to steadily increase my ownership stake.

The dividend is a somewhat paltry 1%, and it hasn't been raised in a decade. But still, the ability to do so is there.

In short, it all comes down to Robert Ingle, and he hasn't been too inclined to do much of anything to crystalize value. But, on the other hand, he's not a dumb guy. He could be plotting something behind the scenes.

The bottom line

Ingles shares are some of the cheapest in North America, especially if you believe the operating company recovers from the hurricane.

Combine that with the massive hidden value in the real estate portfolio, and the conclusion should slap you in the face. There's value here.

The problem is Bobby Ingle. Will he ever do what needs to be done to crystalize some of that value? Or will it have to wait for 20-25 years until he's too old to work anymore? Nobody really knows.

But there's still a good chance this one works out, even without that catalyst. The company has grown earnings over time, and should continue to do so. They have nice stores that are well-located in an area of the country that's growing. They plan to open new stores over time, too. As an operating company, it's not so bad.

One more thing…

This is an example of the deep research that’s shared with premium Canadian Dividend Investing subscribers. We dig deep to discover unknown companies, analyzing them on a fundamental level. That’s where the good stuff is.

But we’re not just limited to small-caps. We scour every corner of the market and look for opportunities that are missed, ignored, or just plain misunderstood. If a stock offers decent value — and a dividend, we insist on it — then it’s worthy of examination. No matter what size it is.

Like the stock I bought over the last week, an excellent long-term winner offering an opportunity amid what should be temporary bad news.

We also looked at a Canadian blue-chip, a stock that makes products I guarantee everyone reading has heard of. It’s in the middle of an interesting transformation that’s been almost completely ignored by the market, a change that has the potential to be massively positive.

Get these ideas — plus hundreds more in the archives, along with Nelson’s FULL portfolio — straight to your inbox, for less than the price of your daily coffee. I’ll help you take control of your portfolio, suggesting smart, low-risk dividend payers, stocks with potential upside, and that generate income that you can DRIP, reinvest, or spend.

Get Canada’s top dividend analyst on your side. Just $200 for your first year. Upgrade today!